DrugSalesDB Research Note

The Biggest Drug Sales Declines: Patent Cliffs Reshaping Pharma

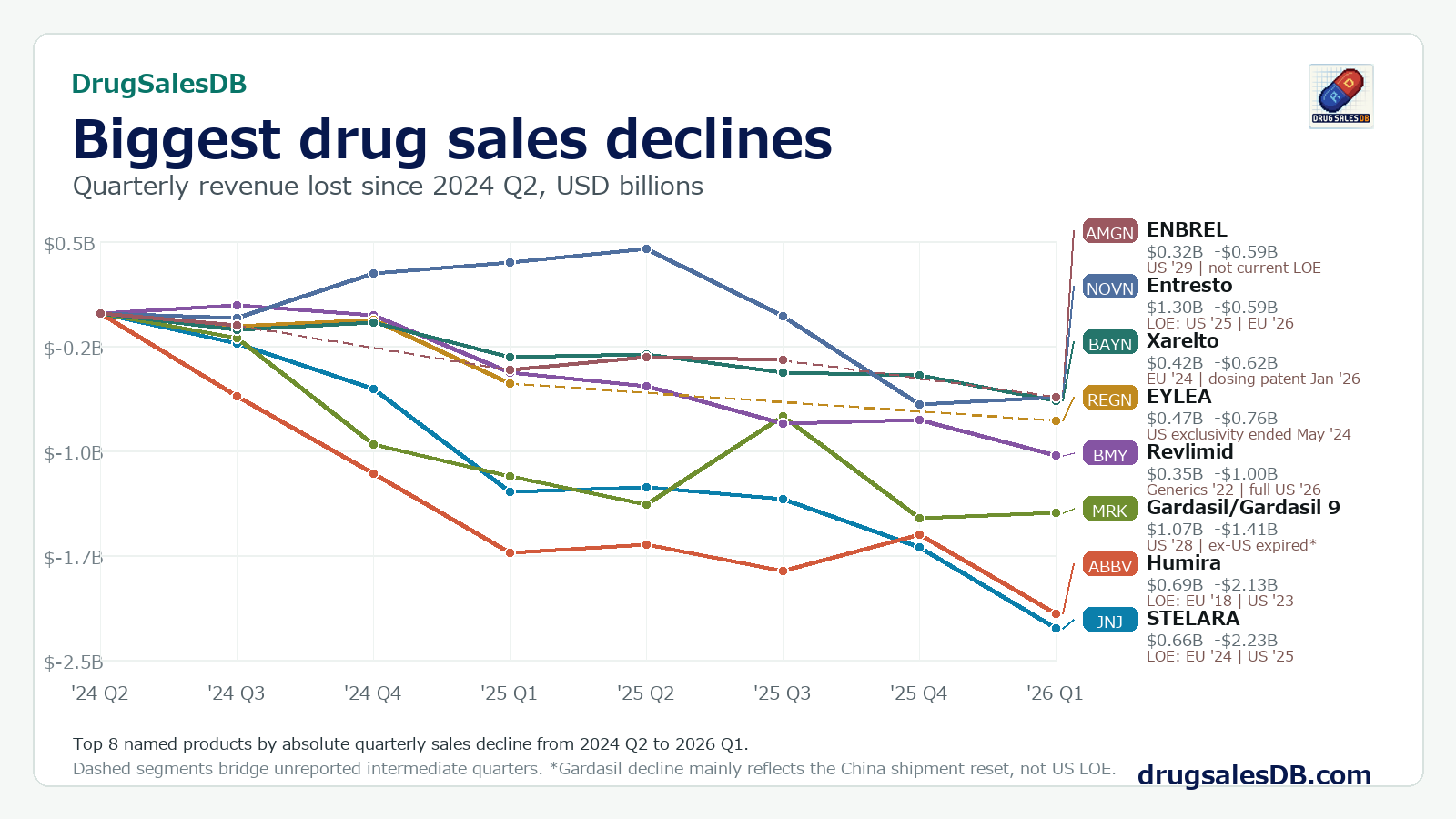

Eight major products lost hundreds of millions - and in some cases billions - in quarterly revenue. The chart reveals classic patent cliffs, a vaccine-market reset, and one important warning against treating every decline as the same story.

Investor takeaway: Stelara and Humira show the clearest biosimilar cliffs. Revlimid, Eylea and Xarelto are further examples of exclusivity loss turning into revenue erosion. Gardasil is different: its drop mainly reflects a China shipment and inventory reset, not an immediate US patent cliff.

The patent cliff is visible quarter by quarter

Annual revenue tables tell investors where a franchise finished. Quarterly product sales show how it got there. In the period from 2024 Q2 to 2026 Q1, Stelara fell by roughly $2.23B per quarter and Humira fell by about $2.13B. Those are not minor mature-product declines. They are the commercial consequences of biosimilar competition arriving in major markets.

The shape matters as much as the endpoint. A smooth decline can reflect ongoing price and share pressure. A sudden step down may indicate generic entry, an inventory correction, or a change in market access. A partial recovery can signal that the original drop was not a simple patent-cliff story.

Stelara, Humira, Revlimid, Eylea and Xarelto show the impact of biosimilar or generic competition.

Gardasil's China shipment and inventory correction produced a sharp decline without a current US patent cliff.

Enbrel illustrates how pricing and market maturity can compress sales even before US biosimilar launch.

Stelara and Humira: the biosimilar cliffs

Stelara was the largest absolute decliner in the chart, moving from about $2.88B in 2024 Q2 to $0.66B in 2026 Q1. European biosimilars arrived first, followed by US competition in 2025. Johnson & Johnson has also cited the Medicare Part D redesign as a headwind. The speed of the decline shows why a blockbuster's final protected quarters can overstate its durable earnings power.

Humira is the industry's best-known biosimilar case. European competition began years earlier, while US biosimilars entered in 2023. Quarterly sales in this dataset fell from about $2.81B to $0.69B over the period. AbbVie's investment case therefore depends less on defending Humira and more on whether newer products, notably Skyrizi and Rinvoq, can replace the lost revenue.

Revlimid, Eylea and Xarelto: different versions of the same pressure

Revlimid is the textbook generic cliff. Licensed generic competition began in 2022, with volumes expanding over time. Its quarterly sales fell from roughly $1.35B to $0.35B in the chart, and US generic restrictions ended in early 2026.

Eylea lost US regulatory exclusivity in May 2024 and subsequently faced biosimilar competition. Its decline from about $1.23B to $0.47B also reflects a franchise transition: Regeneron is trying to move patients toward higher-dose Eylea HD while competitors fight for the original product's market.

Xarelto shows the geographic complexity of LOE. European patent expiry and the end of additional dosing protection created a rolling decline rather than one universal cliff date. Bayer's reported quarterly revenue in the dataset fell by about $0.62B across the period.

Entresto: watching a cliff arrive in real time

Entresto is especially instructive because its sales rose before they fell. The heart-failure drug reached a higher quarterly peak during the period, then declined as US generic entry began in 2025 and European expiry approached in 2026. A strong pre-LOE growth rate can delay the visible damage, but it does not remove the exclusivity risk.

For investors, the relevant number is not only the revenue lost from the starting quarter. It is the gap between the product's peak quarterly contribution and the revenue that remains after competition begins.

Gardasil is the warning label

Gardasil/Gardasil 9 recorded the third-largest decline in this screen, falling by roughly $1.41B per quarter. Calling that a straightforward patent cliff would be wrong. Merck's US protection extends beyond the period shown. The main driver was a sharp reduction in shipments to China after excess channel inventory built up.

This distinction matters. A patent cliff is structurally difficult to reverse because competitors can permanently change pricing and market share. An inventory or distribution correction may still be painful, but its duration and recovery path are different. Product-sales data is most useful when the chart triggers the question, not when the chart is mistaken for the answer.

The eight biggest decliners

| Product | 2024 Q2 | 2026 Q1 | Change | LOE or main context |

|---|---|---|---|---|

| Stelara | $2.88B | $0.66B | -$2.23B | EU 2024; US 2025 |

| Humira | $2.81B | $0.69B | -$2.13B | EU 2018; US 2023 |

| Gardasil | $2.48B | $1.07B | -$1.41B | China shipment reset; US patent 2028 |

| Revlimid | $1.35B | $0.35B | -$1.00B | Generics from 2022; broader US entry 2026 |

| Eylea | $1.23B | $0.47B | -$0.76B | US exclusivity ended May 2024 |

| Xarelto | $1.03B | $0.42B | -$0.62B | EU 2024; dosing patent January 2026 |

| Entresto | $1.90B | $1.31B | -$0.59B | US 2025; EU 2026 |

| Enbrel | $0.91B | $0.32B | -$0.59B | Pricing and maturity; US protection to 2029 |

Values are company-reported quarterly product sales standardized to USD and rounded for readability.

What pharma investors should track next

- Replacement growth versus cliff speed: the key company-level question is whether newer products are adding revenue faster than legacy products are losing it.

- Peak-to-current decline: starting-quarter comparisons can understate damage when a product peaked later in the period.

- Geographic LOE timing: a drug can retain protection in one market while already facing generics or biosimilars elsewhere.

- Volume, price and inventory: identical revenue curves can have very different causes and therefore different investment implications.

A patent cliff does not automatically make a pharmaceutical company unattractive. It changes the burden of proof. The company must show that its launch portfolio, label expansions and pipeline can outrun the decline.

Common questions

Which blockbuster drugs have the largest sales declines?

In this DrugSalesDB period, Stelara and Humira had the largest absolute quarterly revenue declines among the products analyzed. Gardasil, Revlimid, Eylea, Xarelto, Entresto and Enbrel followed.

Why are Humira and Stelara sales falling?

Both products face biosimilar competition after losing exclusivity in major markets. Competitors pressure price and market share, creating the classic patent-cliff curve.

Is Gardasil's decline caused by patent expiry?

Not primarily. The decline shown here mainly reflects lower China shipments after excess channel inventory, while US patent protection remains in place beyond the chart period.

What does LOE mean in pharma?

LOE means loss of exclusivity: the expiry of patent or regulatory protection that had blocked generic or biosimilar competition.

Primary company sources

Context was checked against company filings and reports from Johnson & Johnson, AbbVie, Merck, Bristol Myers Squibb, Regeneron, Bayer, Novartis and Amgen.

See the full quarterly product-sales history

DrugSalesDB includes the standardized spreadsheet and an offline interactive dashboard for comparing product revenue across companies, quarters and therapeutic areas.